On March 17, 2023, CorpFin updated several Compliance and Disclosure Interpretations (C&DIs) related to tender offers. The updates address a wide range of questions. For example, one of the C&DIs clarifies that a tender offer may be subject to conditions only when the conditions are based on objective criteria. Other examples discuss who is a bidder in the tender offer process. You can find the updated C&DIs here.

All posts by George Wilson

Chief Accountant Address Responsibilities of Lead Auditors

On March 17, 2023, Chief Accountant Paul Munter issued a Statement titled “Responsibilities of Lead Auditors to Conduct High-Quality Audits When Involving Other Auditors.” In the Statement, Mr. Munter notes that:

“In 2021, for example, 26 percent of all issuer audit engagements and 57 percent of large accelerated filer audits involved the use of other auditors by the lead auditor.”

The Statement begins with a summary of shortcomings the Office of the Chief Accountant has observed in audit engagements where another auditor is involved. These include using other auditors who are not registered with the PCAOB, failure to communicate the correct legal entity name of other firms, and providing audit committees incomplete information about network firms. The Statement then addresses:

-

- The importance of quality control processes when other auditors play a role in an engagement,

- Roles of network firms,

- Independence considerations, and

- Good practices for audit committees and issuers.

In his conclusion, Mr. Munter states:

“The relevant risks should be considered and the appropriate PCAOB standards must be applied in order to strengthen lead auditors’ supervision over the work of other auditors, within and outside of network firms, to help enhance audit quality.”

As always, your thoughts and comments are welcome!

SEC Enforces for Misleading Non-GAAP Measures and Deficient Disclosure Controls and Procedures

On March 14, 2023, the SEC announced a settled enforcement action against DXC Technology Company (DXC) based on misleading non-GAAP measures and related ineffective disclosure controls and procedures. The company disclosed non-GAAP net income and non-GAAP diluted EPS measures that were adjusted for “transaction, separation and integration-related costs (TSI costs),” which were described as costs related to the merger that formed the company. DXC’s disclosures, as required by regulation S-K Item 10(e), about why the measures provided useful information to investors stated:

“We present these non-GAAP financial measures to provide investors with meaningful supplemental financial information, in addition to the financial information presented on a GAAP basis. Non-GAAP financial measures exclude certain items from GAAP results which DXC management believes are not indicative of core operating performance. DXC management believes these non-GAAP measures allow investors to better understand the financial performance of DXC exclusive of the impacts of corporate wide strategic decisions. DXC management believes that adjusting for these items provides investors with additional measures to evaluate the financial performance of our core business operations on a comparable basis from period to period.”

However, according to the SEC’s order:

“DXC materially increased its non-GAAP earnings by negligently misclassifying tens of millions of dollars of expenses as TSI costs and improperly excluding them in its reporting of non-GAAP measures.”

The SEC’s order goes on to state that the company’s disclosure controls and procedures were inadequate to assure that “the company’s expense classifications were consistent with its own public description of TSI costs.” As a result, non-GAAP net income and non-GAAP diluted EPS were materially overstated in several quarters. The order contains a very revealing look into discussions about this issue between the company’s controllership group and its former Assistant Corporate Controller for External Reporting.

DXC consented to a cease-and-desist order and will pay an $8 million penalty. In addition, the company entered into undertakings to design and implement appropriate non-GAAP measure policies and disclosure controls and procedures.

The use of non-GAAP measures has consistently been at or near the top of frequent SEC comment areas, and this case is a clear indicator that the Enforcement Division is also focused on misuse of non-GAAP measures.

As always, your thoughts and comments are welcome.

A Proxy Area for Care – Perks Reporting!

We have blogged several times about the SEC Enforcement Division’s frequent perks enforcement actions and the messages they send. Among the companies where the SEC has found problems identifying and disclosing perks are:

-

- Gulfport – February 2021

- ProPetro Holding Corp – November 2021

- National Beverage – August 2021

- Hilton – September 2020

- ARGO Group Holdings – June 2020

- Sito Mobile –August 2019

- Dow – July 2018

- Energy XXI – July 2018

- Provectus – December 2017

- MusclePharm – September 2015

- Tyson Foods – April 2005

- GE – September 2004

On March 2, 2023, the Division announced its latest perks-related cases against The Greenbrier Companiesand its founder and former CEO, William A. Furman. Both cases dealt with failure to disclose perks of approximately $329,000 and failure to disclose related-party transactions in which Greenbrier paid Furman for the use of his private airplane. According to the Greenbrier Order, the company lacked appropriate internal controls to identify and record perks and related-party transactions. As a result, both the company’s proxy statements and Form 10-K reports contained material misstatements.

In the Greenbrier Order, the SEC noted that the company undertook significant remedial actions. Greenbrier and Furman both entered into cease-and-desist orders. The company paid a $1,000,000 penalty and Furman paid a $100,000 penalty.

Perks identification and disclosure are clearly areas where financial reporting management and disclosure committees should review company policies, ensure that appropriate controls are designed and operating effectively, and carefully review related disclosures.

As always, your thoughts and comments are welcome!

A Two for One Enforcement – Whistleblower Restrictions and Human Capital Resources Disclosure Controls

On February 3, 2023, the SEC announced a settled enforcement action against Activision Blizzard, Inc. that involved two issues:

-

- Provisions in separation agreements that violated whistleblower protection rules, and

- Ineffective disclosure controls and procedures for human capital resources disclosures.

Activision agreed to pay a $35 million fine and entered into a cease and desist order.

Separation agreement and employment contract provisions that try and limit whistleblowing are not a new enforcement topic. Over the years the SEC has brought cases against a number of companies, including Brinks, KBR, Blackrock and Homestreet, for provisions in agreements that attempt to limit whistleblowing.

Section 21F of the Dodd-Frank Act, “Whistleblower Incentives and Protection”, includes provisions to protect whistleblowers. Pursuant to this section of the Act, the SEC adopted Rule 21F-17, which includes this language:

(a) No person may take any action to impede an individual from communicating directly with the Commission staff about a possible securities law violation, including enforcing, or threatening to enforce, a confidentiality agreement . . . with respect to such communications.

Activision Blizzard routinely included provisions in separation agreements that required departed employees to notify Activision Blizzard if the SEC sent them a request for information, in violation of these rules.

The second issue in this case, inadequate disclosure controls and procedures, relates to Activision Blizzard not having processes and controls to accumulate and communicate information concerning employee complaints about workforce misconduct. The company was aware that its ability to attract, retain, and motivate employees was a particularly important risk in its business. It included this language as a risk factor heading in 10-Ks for 2017, 2018, 2019 and 2020:

“If we do not continue to attract, retain, and motivate skilled personnel, we will be unable to effectively conduct our business.”

According to the SEC’s Order, the company:

“lacked controls and procedures designed to ensure that it captured and assessed – from a disclosure perspective – certain information related to these risk factors.”

The SEC specifically focused on information about workplace misconduct. As a result, according to the SEC’s Press Release, the company

“lacked sufficient information to understand the volume and substance of employee complaints about workplace misconduct and did not assess whether any material issues existed that would have required public disclosure.”

You can read more details in the SEC’s Order.

As always, your thoughts and comments are welcome!

New Rule 10b5-1 Questions Abound

The SEC’s December 14, 2022, Final Rule “Insider Trading Arrangements and Related Disclosures” dramatically changed the landscape for using Rule 10b5-1 plans.

One of the major questions the new rule raises is “what is a non-Rule 10b5-1 trading plan?” Gary Brown, Partner, Nelson Mullins and SEC Institute workshop leader and author, and his colleague Charles Vaughn, Partner, Nelson Mullins, address this question and the issues it raises in their firm’s securities alert titled “To be or not to be a “non-Rule 10b5-1 trading arrangement” – that is the question!”

You can also learn about these required changes in PLI’s related One-Hour Briefings:

SEC Amendments to Rule 10b5-1 and Related Disclosure Requirements (on-demand)

Rule 10b5-1 Amendments – More Than Meets the Eye – Implementation Conundrums and Disclosure Challenges (scheduled for March 23, 2023)

As always, your thoughts and comments are welcome!

A Few Form 10-K Tips and Reminders

In the spirit of being helpful and at the risk of being a bit repetitive, this earlier blog post discusses a number of frequent Form 10-K errors to avoid and new areas to address. Included are issues such as where to place the S-K Item 201(d) equity compensation plan information (Item 12) and making sure Item 6 is labeled “Reserved.”

Also, don’t forget to include the two new clawback related check boxes on your cover page. You can read more in this post.

As always, your thoughts and comments are welcome!

Disclosures and Form Changes for the “Recovery of Erroneously Awarded Compensation” a/k/a “Clawback” Rules

As we discussed in this earlier post, the SEC’s October 2022 “Listing Standards for Recovery of Erroneously Awarded Compensation” rules will require companies whose securities are listed on national securities exchanges to develop and adopt policies for the recovery or “clawback” of incentive compensation that has been “erroneously awarded” when a company restates its financial statements. The Dodd-Frank Act required the SEC to implement these requirements through listing standards that national securities exchanges will soon be required to adopt.

Based on the final rules’ January 27, 2023, effective date, the timetable for implementation of the clawback rules, including the adoption of a clawback policy by exchange-listed companies, will be:

-

- February 26, 2023 – last day by which national securities exchanges are to file proposed clawback listing standards;

- November 28, 2023 – last day by which clawback listing standards must become effective; and

- January 27, 2024 – last day by which listed companies must adopt and comply with an appropriate clawback policy.

Of course, if the exchange listing standards become effective earlier than the November 28, 2023 deadline, companies will have to adopt policies before January 27, 2024.

This earlier post discusses the implementation process in more detail and includes a policy template to help companies get a head start in this process.

This current post reviews the rules’ new disclosures:

-

- First, if during or after the last completed fiscal year, a company is required to prepare an accounting restatement that requires recovery of “erroneously awarded” compensation, or, as of the last completed fiscal year, there was an outstanding balance of “erroneously awarded compensation” still to be recovered from a prior restatement, the required disclosures include:

- The date of the restatement;

- The dollar amount of compensation required to be clawed back;

- Details of the calculation of compensation subject to clawback;

- If the financial reporting measure in a compensation plan subject to clawback related to a stock price or total shareholder return, details of the estimates used in determining clawback amounts and the methodology used for these estimates;

- The dollar amount of any “erroneously awarded compensation” outstanding at the end of the last completed fiscal year; and

- If the dollar amount of compensation subject to clawback has not yet been determined, disclose this information, including an explanation of why the amount could not be determined. The required information should then be disclosed in the next report requiring compensation disclosure pursuant to Item 402 of Regulation S-K.

- Second, when a company determines, based on the limited practicability exceptions in the rules, that clawback would be impracticable, it must disclose the amount of the compensation recovery not pursued for each executive officer and all executive officers as a group, along with a description of why recovery was not pursued.

- Third, disclosure must include amounts that, as of the end of the most recently completed fiscal year, have been outstanding for 180 days or more from any current or former named executive officer.

- Fourth, if a company has a restatement and concludes that clawback of compensation is not required for that restatement, it must disclose how it arrived at that conclusion.

In addition to the disclosures described above, each listed company must file its clawback policy as Exhibit 97 to Form 10-K. These new disclosures are to be tagged with Inline XBRL and will also be required in Forms 20-F and 40-F. Note that this will not be required until after the company is required to adopt a clawback policy, which could be as late as January 27, 2024.

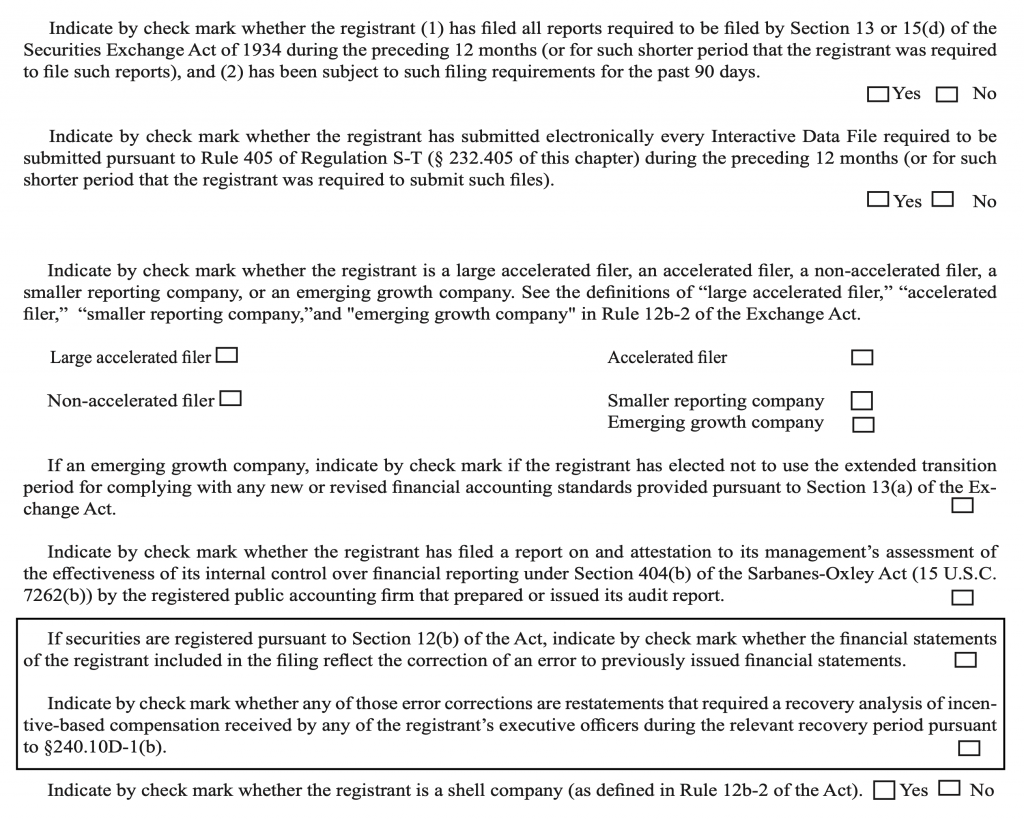

Furthermore, the rules add two new checkboxes to the cover pages of Form 10-K, Form 20-F and Form 40-F. These forms were updated on January 27, 2023, the effective date of the new rules. Below is the revised section of the cover page of Form 10-K from the SEC’s webpage:

Also, on January 31, 2023, the staff issued several new C&DIs addressing these new disclosures. One of the C&DIs addresses the form amendments:

Question 104.19

Question: The form amendments adding check boxes to the cover page of Form 10-K, Form 20-F, and Form 40-F indicating whether the form includes the correction of an error in previously issued financial statements and a related recovery analysis are effective January 27, 2023. However, the listing standards are not required to be effective until November 28, 2023 and issuers subject to such listing standards will not be required to adopt a recovery policy for 60 days following the date on which the applicable listing standards become effective. Will issuers be required to mark the check boxes in 2023 before an issuer is required to adopt a recovery policy and comply with the applicable listing standards?

Answer: In the adopting release, the Commission indicated that it does not expect compliance with the disclosure requirements until issuers are required to have a recovery policy under the applicable exchange listing standard. While the check boxes and other disclosure requirements will be in the rules and forms in 2023, we do not expect issuers to provide such disclosure until they are required to have a recovery policy under the applicable listing standard. [January 31, 2023]

Because disclosure is not required until after a listed company is required to adopt a clawback policy, whether to add the new checkboxes on the cover page of your annual report is essentially an “it depends” decision. We believe that the better practice is to include the new checkboxes as they are now on the official form. Some companies, however, may decide not to include them since the underlying disclosure requirement is not effective until after the company is required to adopt a clawback policy. Assuming that the EDGAR system allowed such a submission, that would, in essence, make both answers allowable.

Non-listed companies have similar considerations about inclusion of the checkboxes on the form cover but they will not have to check either of the boxes. The first box would not apply – they do not have “Section 12(b)” (i.e., listed) securities. Then, even if they had a restatement, the second box would not apply because it would not be “required.” Should non-listed companies not have a clawback policy – we’re not saying that adoption of a clawback policy might not be a wise move as a matter of good governance practices. But even if they do – these rules will not apply to them.

As always, your thoughts and comments are welcome!

Getting Ahead of the MD&A Update Curve – Meaningfully Addressing Liquidity and Capital Resources Disclosures

As we discussed in a prior post, three parts of the SEC’s 2020 MD&A modernization have become focus areas in the comment process:

-

- Critical accounting estimate disclosures

- Quantitative and qualitative disclosures about material changes

- Meaningfully addressing liquidity and capital resources disclosures

We also explored how one of the reasons behind this increase in MD&A comments could be that companies are reluctant to change MD&A, even when the change is to comply with a new rule or to improve MD&A!

In earlier posts we explored comment letter exchanges focused on critical accounting estimate disclosures and quantitative and qualitative disclosures about material changes.

Today’s post examines an example comment and company response for the third of these three areas, meaningfully addressing liquidity and capital resources disclosures.

The Regulation S-K Item 303 guidance for this disclosure is very big picture:

Analyze the registrant’s ability to generate and obtain adequate amounts of cash to meet its requirements and its plans for cash in the short-term (i.e., the next 12 months from the most recent fiscal period end required to be presented) and separately in the long-term (i.e., beyond the next 12 months). The discussion should analyze material cash requirements from known contractual and other obligations.

……..

Describe the registrant’s material cash requirements, including commitments for capital expenditures, as of the end of the latest fiscal period, the anticipated source of funds needed to satisfy such cash requirements and the general purpose of such requirements.

It is important to note that the language “cash requirements” does not limit the disclosure to contractual obligations, but all reasonably likely cash requirements. This in essences is a discussion of how the business is funded in both the long- and short-term. An important part of this analysis is clear and understandable disclosure about sources of cash and how they have varied in the past and how they could vary in the future.

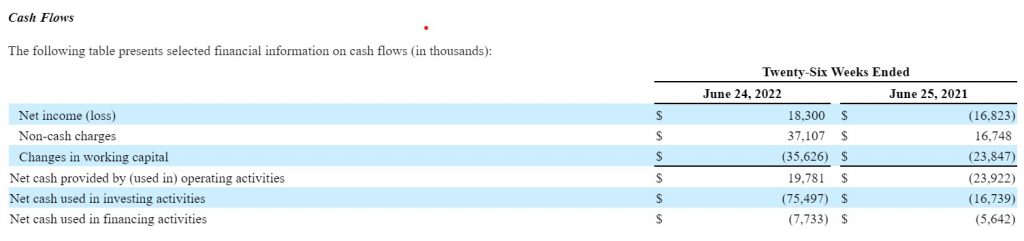

Here is an example disclosure from a company’s Form 10-Q MD&A that generated a comment to provide more meaningful disclosure about how cash is generated:

Net cash provided by operations was $19.8 million for the twenty-six weeks ended June 24, 2022 consisting of a net income of $18.3 million and $37.1 million of non-cash charges, partially offset by investments in working capital growth of $35.6 million. Non-cash charges increased $20.4 million primarily due to a $12.8 million change in deferred tax expenses and a $5.0 million increase in changes in the fair value of earn-out liabilities. The cash used for working capital growth of $11.8 million is primarily driven by the Company’s reinvestment in working capital to support sales growth.

The SEC’s comment focuses on more robust explanations for the causal factors behind changes in cash from operating activities:

Liquidity and Capital Resources Cash Flows, page 2

-

- Your analysis of changes in operating cash flows references net results, noncash charges and working capital. Note that references to these items may not provide a sufficient basis to understand how operating cash actually was affected between periods. Your analysis should discuss factors that actually affected operating cash and reasons underlying these factors. In connection with this, discuss more fully what the cash used for working capital growth primarily driven by the Company’s reinvestment in working capital to support sales growth represents and the potential for this to be a continuing trend. Refer to the introductory paragraph of section IV.B and paragraph B.1 of Release No. 33-8350 for guidance, and section 501.04 of the staff’s Codification of Financial Reporting Releases regarding quantification of variance factors. Please revise your disclosure as appropriate.

In its response, the company provided more detailed discussion about the causal factors behind the change in operating cash flows:

In response to the Staff’s comment the Company will expand its disclosure of the factors impacting operating cash flows in future filings. The following is an example of the future disclosure related to operating cash flows:

Net cash provided by operations was $19.8 million for the twenty-six weeks ended June 24, 2022, compared to net cash used in operating activities of $23.9 million for the twenty-six weeks ended June 26, 2021. The increase in cash provided by operating activities is primarily due to the increased net income, net of non-cash charges, in the current year of $55.4 million versus a loss of $0.1 million in the prior year period. This improvement in cash-based profitability is primarily due to a 65% increase in sales compared to the prior year period. The sales growth also resulted in higher working capital (increased accounts receivable and inventory partially offset by higher accounts payable). The working capital growth of $11.8 million versus the prior year period partially offset the favorable impact of increased profitability. The Company’s increased working capital investment in the current year is the result of rapid sales growth driven by the Company’s recovery from the pandemic. The Company expects working capital growth to moderate in the future as sales growth normalizes.

Each of the three MD&A areas addressed in our “Getting Ahead of the MD&A Update Curve” series was changed in the SEC’s 2020 modernization rule, which has been in effect for two years. SEC comments, like those discussed in this series, can be easily avoided by assuring your MD&A appropriately addresses each area.

As always, your thoughts and comments are welcome!

CorpFin Addresses Pay Versus Performance Questions with Compliance and Disclosure Interpretations

On February 10, 2023, CorpFin issued 15 Compliance and Disclosure Interpretations (C&DIs) to address issues arising in preparing the Pay Versus Performance disclosures adopted in August 2022. Given that the new disclosures are required in proxy and information statements that include Regulation S-K Item 402 disclosures for fiscal years ending on or after December 16, 2022, the C&DIs are very timely!

In addition to other topics, the new C&DIs

-

- Answer questions about the computation of tabular information required in pay versus performance disclosures;

- Clarify that pay versus performance information is not required in Form 10-K;

- Provide guidance for disclosing details of the adjustments to arrive at compensation actually paid; and

- Discuss considerations in selecting financial performance measures.

As a reminder, in this post, you can find a template for preparation of pay versus performance disclosures from Gary Brown of Nelson Mullins.

As always, your thoughts and comments are welcome!