In its June 30, 2025, Form 10-Q, Getty Images Holdings, Inc. made this disclosure in the Liquidity and Capital Resources section of their MD&A:

Operating Activities

Cash provided by operating activities is primarily comprised of net income, as adjusted for non-cash items, and changes in operating assets and liabilities. Non-cash adjustments consist primarily of depreciation and amortization, unrealized gains and losses on our foreign denominated debt, equity- based compensation and deferred income taxes.

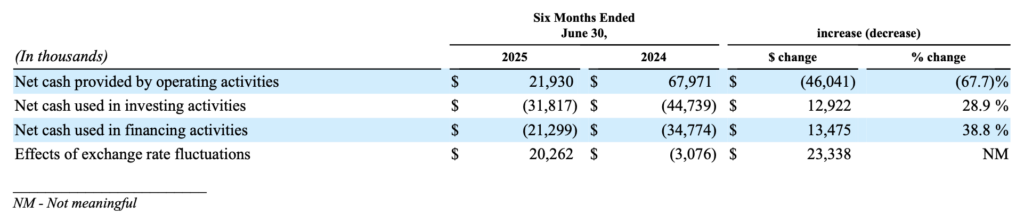

For the six months ended June 30, 2025 cash provided by operating activities was $21.9 million, as compared to cash provided by operating activities of $68.0 million for the six months ended June 30, 2024. The decrease in cash provided by operating activities was primarily driven by merger related costs.

In a comment letter dated September 26, 2025, the SEC focused on one of their frequent liquidity and capital resources comment issues:

Liquidity and Capital Resources. – Operating Activities, page 35

Please provide a more informative analysis and discussion of changes in cash flows, including changes in working capital components, for each period presented. In doing so, explain the underlying reasons and implications of material changes between periods to provide investors with an understanding of trends and variability in cash flows from operating activities. Ensure your discussion and analysis is not merely a recitation of changes evident from the financial statements. Refer to Item 303(a) of Regulation S-K and sections IV.B and IV.B.1 of SEC Release No. 33-8350.

In their response letter dated October 9, 2025, Getty Images provided this example of expanded disclosure:

For the six months ended June 30, 2025, cash provided by operating activities was $21.9 million, as compared to cash provided by operating activities of $68.0 million for the six months ended June 30, 2024. The decrease in cash provided by operating activities was primarily driven by merger related costs, of which $26.3 million were paid in the six-month period ending June 30, 2025. These costs were comprised mainly of professional services fees, including legal, advisory, accounting and tax fees. In addition, our cash provided by operating activities was impacted by changes in working capital, including reduced cash flows from the change in timing of collections of accounts receivable and the payments of accrued expenses, increased cash flows from the timing of payments for accounts payable and interest, changes in deferred revenue and an increase in cash paid for taxes of $5.6 million for the six months ended June 30, 2025 as compared to the six months ended June 30, 2024

This discussion of the drivers of cash flow versus a mechanical recitation of operating cash flow reconciling items provides much more useful information.

As always, your thoughts and comment are welcome!