In its Form 10-Q for the quarter ended June 30, 2025, The Goodyear Tire & Rubber Company disclosed that it had identified errors in its previously issued financial statements related to the historical currency remeasurement of its operations in Turkey, which had been designated a highly inflationary economy beginning April 1, 2022:

NOTE 16. REVISION OF PREVIOUSLY ISSUED FINANCIAL STATEMENTS

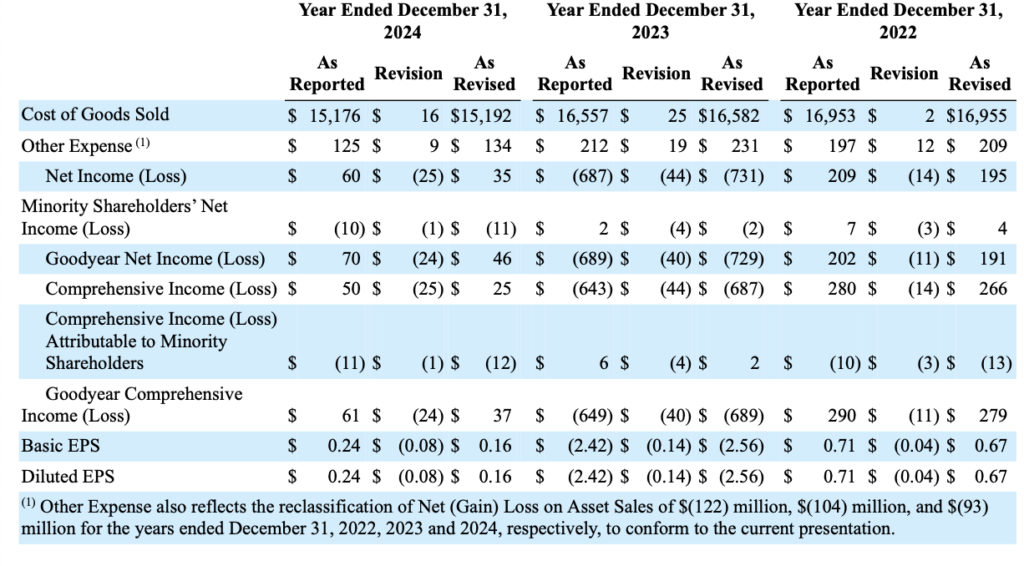

As discussed in Note 1, in preparing the consolidated financial statements as of and for the three and six months ended June 30, 2025, we identified errors in our previously issued financial statements related to our historical computation of currency remeasurement of our foreign operations in Turkey, which was designated as a highly inflationary economy beginning April 1, 2022. The identified errors impacted our previously issued 2022, 2023 and 2024 annual and interim financial statements. The impact of the errors on the previously issued consolidated statements of operations and comprehensive income for the quarter ended March 31, 2025 were de minimis. There were no impacts on previously reported cash flows from operating, investing and financing activities in any prior periods.

We evaluated the errors in accordance with SEC Staff Accounting Bulletin Nos. 99 and 108 and determined that the related impacts were not material in any previously issued annual or interim financial statements. We revised the prior period amounts presented in these financial statements to correct the errors. The applicable notes to the accompanying financial statements have also been corrected to reflect the impact of the revisions of the previously filed consolidated interim financial statements.

The following tables reflect the impact of the revision to the specific line items presented in our previously reported financial information.

Impacts to Consolidated Statements of Operations and Comprehensive Income (in millions, except per share data)

As you might expect with this type of revision, the SEC asked Goodyear about related ICFR implications in a comment letter dated September 10, 2025:

Form 10-Q for the Period Ended June 30, 2025

Notes to Consolidated Financial Statements

Note 16. Revision of Previously Issued Financial Statements, page 33

-

- We note your disclosure that you identified and corrected immaterial errors related to your historical presentation of your foreign operations in Turkey. Please tell us further details of the error, including, but not limited to, a discussion of who identified the error, when, and how, and whether it was the result of any control deficiency. In your response ensure you include a thorough discussion and description of the control deficiency to the extent one was identified, the Company’s evaluation of whether it was a control deficiency, significant deficiency, or material weakness, and any remediation plans. To the extent the Company concluded there was not a control deficiency, tell us why.

As you can read in the company’s September 23, 2025 response letter, Goodyear explained that the error was identified during second-quarter 2025 close procedures. The issue arose from a manual process used to remeasure inventory and accounts payable balances in Turkey following that country’s designation as highly inflationary.

Management concluded that the root cause was a design deficiency—specifically, the lack of an effectively designed control to verify that manually translated balances agreed to the general ledger.

Importantly, Goodyear evaluated the deficiency under the SEC’s internal control framework and concluded:

- The deficiency was limited to Turkey, which represented approximately 2% of consolidated revenues and less than 1% of consolidated assets in the affected years.

- The impact was confined to inventory and accounts payable in Turkey.

- It was not reasonably possible that the potential misstatement could be larger than the actual error identified.

- There were no broader indicators of pervasive control failures or fraud.

Based on this analysis, the company determined that the issue constituted a significant deficiency, but not a material weakness, and that its internal control over financial reporting remained effective.

Goodyear also implemented a remediation plan that included redesigning the balance sheet remeasurement control to calculate translated Turkey balances and agree them to the U.S. dollar general ledger.

Following its review of Goodyear’s response, the SEC did not issue additional comments. In other words, the Staff accepted the company’s internal control conclusions.

For practitioners, this comment letter underscores the importance of documenting complex judgments contemporaneously and thoroughly.

As always, your thoughts and comments are welcome!