As we approach third quarter-end 2020, many of us will be drafting and reviewing earnings releases. A majority, perhaps most, of these earnings releases will include non-GAAP measures. The SEC includes earnings releases in their review process and, as you likely already know, frequently comments on the use of non-GAAP measures included in these crucial communication documents.

More often than not the issues raised in these comments are areas that are dealt with in Regulation G, S-K Item 10(e), or the related Compliance and Disclosure Interpretations. To help avoid non-GAAP problems in earnings releases and other documents, this series of posts focuses on earnings releases that resulted in SEC comments about the use of non-GAAP measures.

To make this a bit more of a challenge, you can first read the excerpt of the release behind the comment and try to spot the issue. If you prefer, you can read straight through to the comment and explanation that follow.

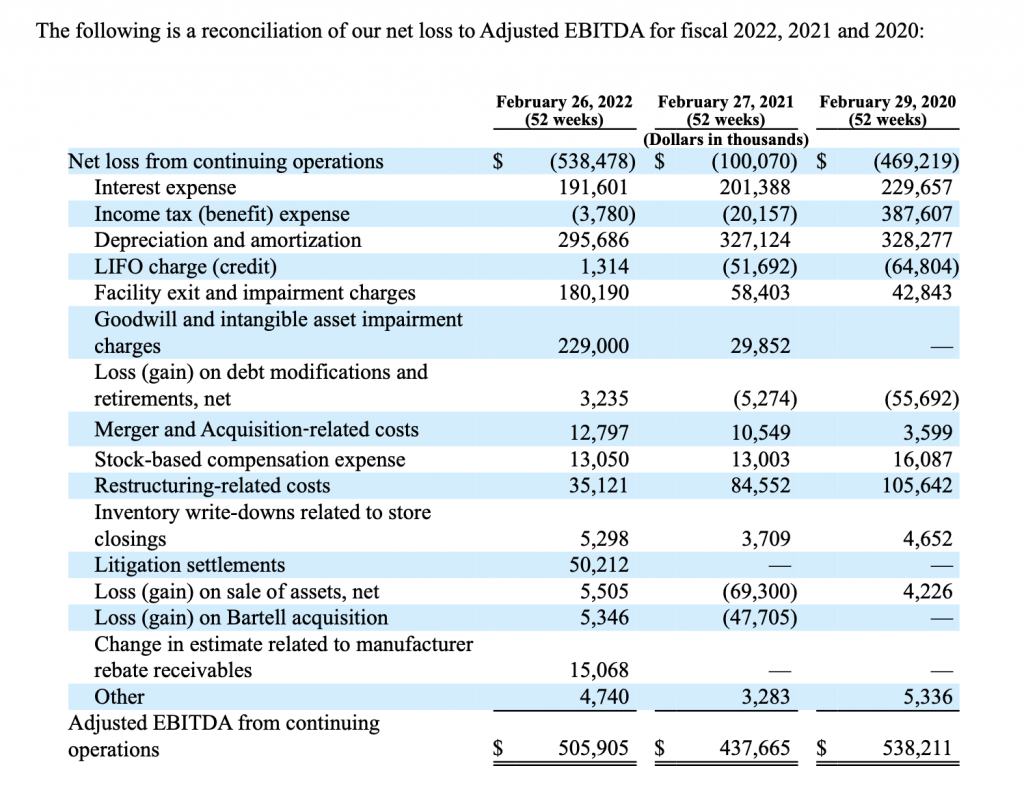

This excerpt is from an 8-K filed by Dasan Zhone Solutions, Inc. on May 7, 2020. Can you spot the non-GAAP issue?

There is a bit of non-GAAP complexity behind the SEC comment on this release. First, as an earnings release, it is essentially subject to Regulation G, the SEC’s non-GAAP guidance for measures not included in filed documents.

However, since an earnings release is required to be furnished (not filed) with the SEC on an Item 2.02 Form 8-K, it is subject to the Form 8-K instructions which include this “hook” to S-K Item 10(e), the SEC’s rules for non-GAAP measures used in a filed document.

Instructions:

The requirements of paragraph (e)(1)(i) of Item 10 of Regulation S-K (17 CFR 229.10(e)(1)(i)) shall apply to disclosures under this Item 2.02.

The part of S-K Item 10(e) that this instruction makes applicable to an earnings release is:

(e) Use of non-GAAP financial measures in Commission filings.

(1) Whenever one or more non-GAAP financial measures are included in a filing with the Commission:

(i) The registrant must include the following in the filing:

(A) A presentation, with equal or greater prominence, of the most directly comparable financial measure or measures calculated and presented in accordance with Generally Accepted Accounting Principles (GAAP);

(B) A reconciliation (by schedule or other clearly understandable method), which shall be quantitative for historical non-GAAP measures presented, and quantitative, to the extent available without unreasonable efforts, for forward-looking information, of the differences between the non-GAAP financial measure disclosed or released with the most directly comparable financial measure or measures calculated and presented in accordance with GAAP identified in paragraph (e)(1)(i)(A) of this section;

(C) A statement disclosing the reasons why the registrant’s management believes that presentation of the non-GAAP financial measure provides useful information to investors regarding the registrant’s financial condition and results of operations; and

(D) To the extent material, a statement disclosing the additional purposes, if any, for which the registrant’s management uses the non-GAAP financial measure that are not disclosed pursuant to paragraph (e)(1)(i)(C) of this section;

This company included non-GAAP measures in the headline of their earnings release without presenting the related GAAP measure with equal or greater prominence. This resulted in this comment:

Form 8-K furnished May 7, 2020 Exhibit 99.1, page 1

- We note your presentation of the non-GAAP measures, Adjusted EBITDA and Net Income (loss) attributable to DZS – Non-GAAP, on page 1 of your earnings release. Please revise to present the most directly comparable GAAP measure (i.e. net loss) with equal or greater prominence to avoid placing undue prominence on the non-GAAP measures. Refer to the guidance outlined in Question 102.10 in the Division of Corporation Finance’s Compliance and Disclosure Interpretations surrounding Non-GAAP Financial Measures.

The C&DI mentioned states:

Question 102.10

Question: Item 10(e)(1)(i)(A) of Regulation S-K requires that when a registrant presents a non-GAAP measure it must present the most directly comparable GAAP measure with equal or greater prominence. This requirement applies to non-GAAP measures presented in documents filed with the Commission and also earnings releases furnished under Item 2.02 of Form 8-K. Are there examples of disclosures that would cause a non-GAAP measure to be more prominent?

Answer: Yes. Although whether a non-GAAP measure is more prominent than the comparable GAAP measure generally depends on the facts and circumstances in which the disclosure is made, the staff would consider the following examples of disclosure of non-GAAP measures as more prominent:

- Presenting a full income statement of non-GAAP measures or presenting a full non-GAAP income statement when reconciling non-GAAP measures to the most directly comparable GAAP measures;

- Omitting comparable GAAP measures from an earnings release headline or caption that includes non-GAAP measures;

- Presenting a non-GAAP measure using a style of presentation (e.g., bold, larger font) that emphasizes the non-GAAP measure over the comparable GAAP measure;

- A non-GAAP measure that precedes the most directly comparable GAAP measure (including in an earnings release headline or caption);

- Describing a non-GAAP measure as, for example, “record performance” or “exceptional” without at least an equally prominent descriptive characterization of the comparable GAAP measure;

- Providing tabular disclosure of non-GAAP financial measures without preceding it with an equally prominent tabular disclosure of the comparable GAAP measures or including the comparable GAAP measures in the same table;

- Excluding a quantitative reconciliation with respect to a forward-looking non-GAAP measure in reliance on the “unreasonable efforts” exception in Item 10(e)(1)(i)(B) without disclosing that fact and identifying the information that is unavailable and its probable significance in a location of equal or greater prominence; and

- Providing discussion and analysis of a non-GAAP measure without a similar discussion and analysis of the comparable GAAP measure in a location with equal or greater prominence. [May 17, 2016]

This is the Company’s response to the comment:

DZS acknowledges the Staff’s comment and will undertake to adjust, in future Forms 8-K related to financial results, the presentation of financial information to ensure that the most directly comparable GAAP measure is presented with equal or greater prominence relative to non-GAAP measures.

Specifically, the Company will include in the headline and table on page 1, with equal or greater prominence, GAAP Net Income (loss) attributable to DZS, as the most directly related GAAP measure to the non-GAAP measures Adjusted EBITDA and Net income (loss) attributable to DZS – Non-GAAP.

As always, your thoughts and comments are welcome!